In This Article

- Why is business travel emissions reporting still broken?

- What makes Scope 3 emissions from business travel so hard to calculate?

- What is CSRD and how does it affect your travel programme?

- How does Cogent turn emissions data into a live intelligence layer?

- What does auditable ESG reporting actually require from your T&E data?

- Manual vs agentic: what do the two approaches actually produce?

- Frequently Asked Questions

It's not that enterprise travel teams lack sustainability ambition. It's that fragmented T&E data makes auditable Scope 3 emissions reporting practically impossible without weeks of manual consolidation. When a board-level net zero target is measured annually, a spreadsheet that is four weeks out of date is not a carbon reporting strategy.

Business travel emissions sit inside Scope 3, Category 6 of the Greenhouse Gas Protocol, the accounting standard used by the vast majority of global enterprises to calculate climate impact. Scope 3 Category 6 covers all business travel by air, rail, ground transport, and hotel stays. It is one of the most visible and measurable emissions categories a company can report on. And yet, for most organisations, it remains one of the hardest to report on accurately.

This article explains why that gap exists, what regulatory pressure is closing it, and how Cogent by PredictX changes the reporting model entirely.

Why is business travel emissions reporting still broken?

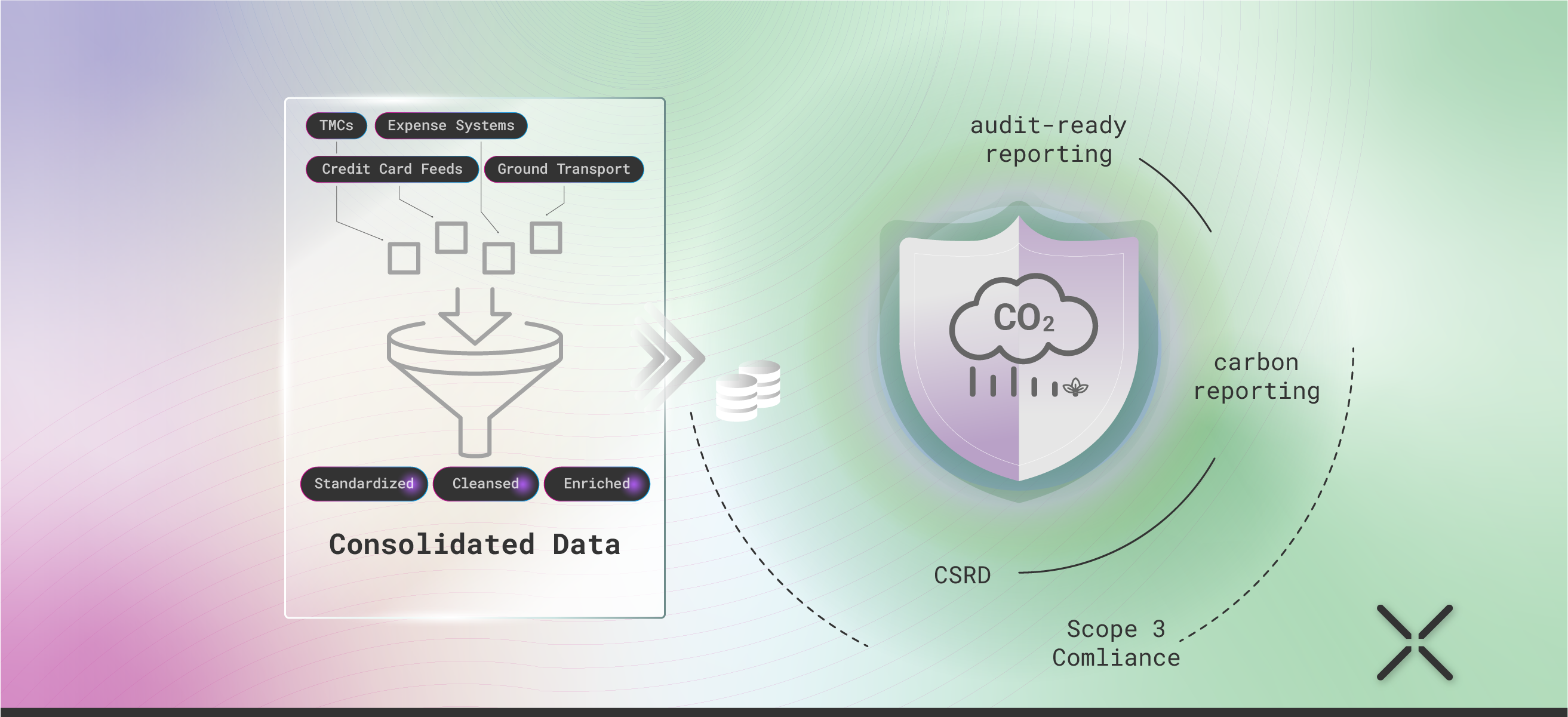

Business travel emissions reporting is broken because the data required to produce it lives across five or more disconnected systems, none of which share a common emissions methodology or update in real time.

Travel management companies (TMCs) hold booking records for managed trips. Corporate card feeds capture unmanaged and out-of-policy spend. Expense platforms hold the receipts. Fleet systems track vehicle mileage separately. Hotel preferred partner programmes report sustainability data, when they report at all, in inconsistent formats. Pulling these together manually takes weeks and introduces systematic error at every consolidation point.

By the time the annual ESG report is ready, the data is already stale, and the methodology used may not align with what the finance team is seeing in the expense system. The sustainability team asks for a carbon footprint. The travel manager gives an apologetic estimate weeks later.

According to research by the GBTA Foundation, over 60% of large enterprises now have board-level sustainability targets that include business travel emissions. Fewer than a quarter can report on them accurately without significant manual effort. And DEFRA's UK GHG Conversion Factors guidance, the emissions factor standard used by thousands of travel programmes, is updated annually, meaning any manual process that hardcodes these factors is out of date within months.

The reporting gap is not a technology problem. It is a data architecture problem. As Cogent CEO Keesup Choe puts it: "You cannot manage what you don't measure accurately. We deliver certified, auditable CO2 emission calculations aligned with frameworks like the GHG Protocol and CSRD."

What makes Scope 3 emissions from business travel so hard to calculate?

Scope 3 emissions from business travel are difficult to calculate because each transport mode uses a different emissions factor methodology, and the data for each mode sits in a separate system with no shared format.

Scope 3 emissions are indirect greenhouse gas emissions produced in a company's value chain, not from its own operations. Category 6 specifically covers employee travel for business purposes. Under the Greenhouse Gas Protocol Corporate Standard, companies are required to account for Scope 3 emissions in their climate disclosures, and business travel is among the categories most commonly included.

Here is what the calculation challenge looks like in practice:

- Air travel uses DEFRA emissions factors that vary by aircraft type, seat class, route distance, and whether radiative forcing is included.

- Hotel stays rely on reported emissions intensity per room night, data that many hotel groups do not publish consistently, and that varies significantly by property.

- Rail travel requires route-level electricity grid emissions factors that differ by country.

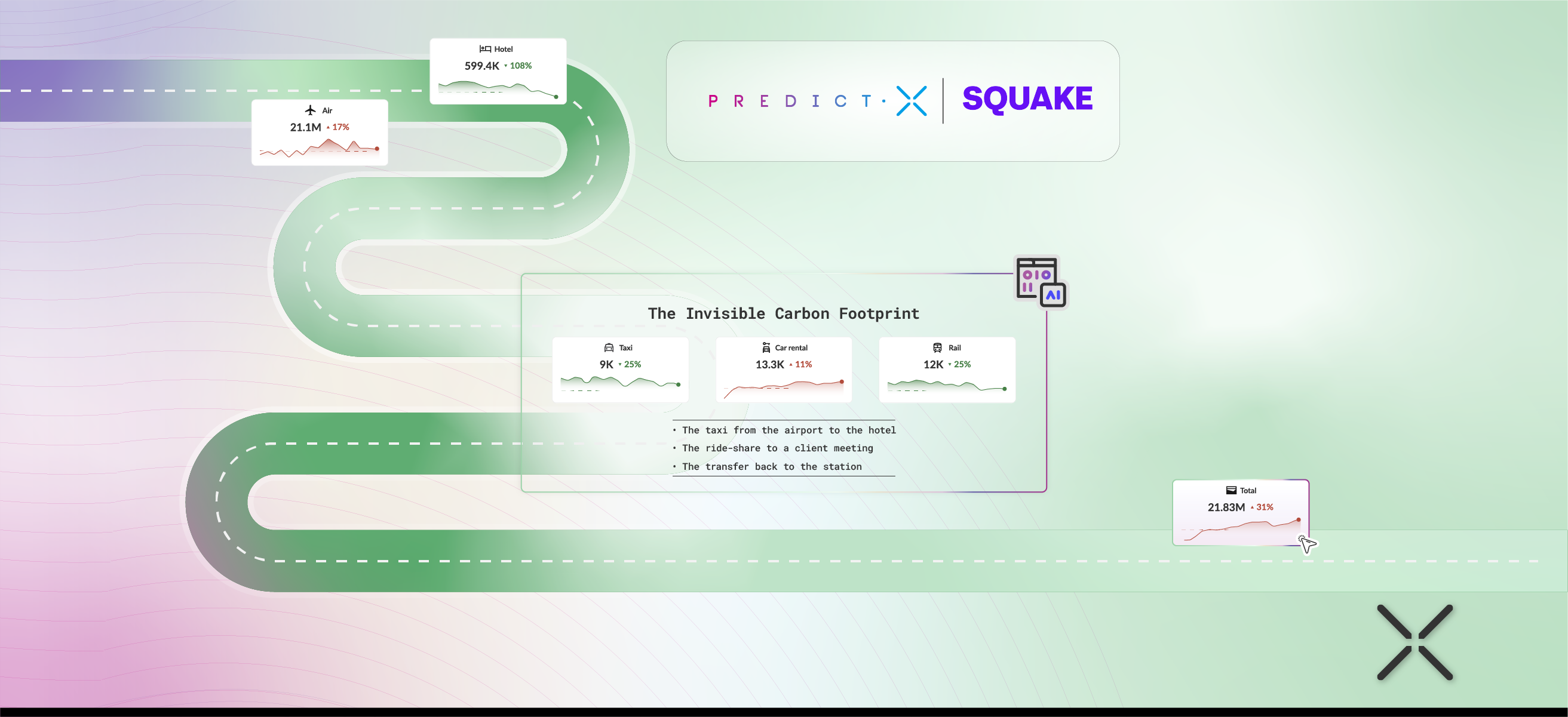

- Ground transport depends on vehicle type, fuel type, distance, and whether it is managed fleet or third-party (taxi, rideshare, rental car).

- Fleet emissions are often tracked in a completely separate system outside the managed travel programme.

No single system holds all of this. No standard maps cleanly across all categories. For multi-entity organisations with operations in multiple countries and different booking channels, the aggregation burden compounds at every level.

A concrete pattern from enterprise deployments: a large global organisation needed to update its emissions calculation methodology mid-year to align with new regulatory guidance. Under a manual reporting process, that change required rebuilding months of historical data from scratch. With an agentic platform running against a unified data layer, the same methodology update is applied retroactively in seconds. The CO2 precision methodology deep dive covers exactly how that calculation layer works in practice.

What is CSRD and how does it affect your travel programme?

The Corporate Sustainability Reporting Directive (CSRD) is EU legislation that requires large companies to publish detailed, auditable sustainability disclosures, including Scope 3 emissions from business travel, as part of their annual reports.

The CSRD entered into force in January 2023 and is being phased in from 2024 through 2028, per the European Commission's official CSRD timeline. It replaces the Non-Financial Reporting Directive (NFRD) and significantly expands both the number of companies in scope and the depth of disclosure required. Under CSRD, business travel emissions are not a voluntary reporting category. They are a required disclosure, verified by an external auditor.

The phasing schedule is broader than many travel teams realise:

The key implications for travel programmes:

- Auditability is mandatory. Emissions data must be traceable to source, consistent in methodology, and reproducible. A manually consolidated spreadsheet cannot show its calculation logic and will not satisfy a CSRD auditor.

- Scope 3 Category 6 is specifically named. Travel managers are now directly in scope of a regulatory disclosure requirement that previously sat only with sustainability teams.

- Non-EU companies with EU operations are affected. Phase 4 brings global multinationals into scope regardless of headquarters location.

The European Financial Reporting Advisory Group (EFRAG) has published detailed European Sustainability Reporting Standards (ESRS) specifying exactly what Scope 3 Category 6 data must include. For a detailed breakdown of how to structure your travel programme data for CSRD compliance, the CSRD Scope 3 business travel compliance guide covers exactly what auditors will check.

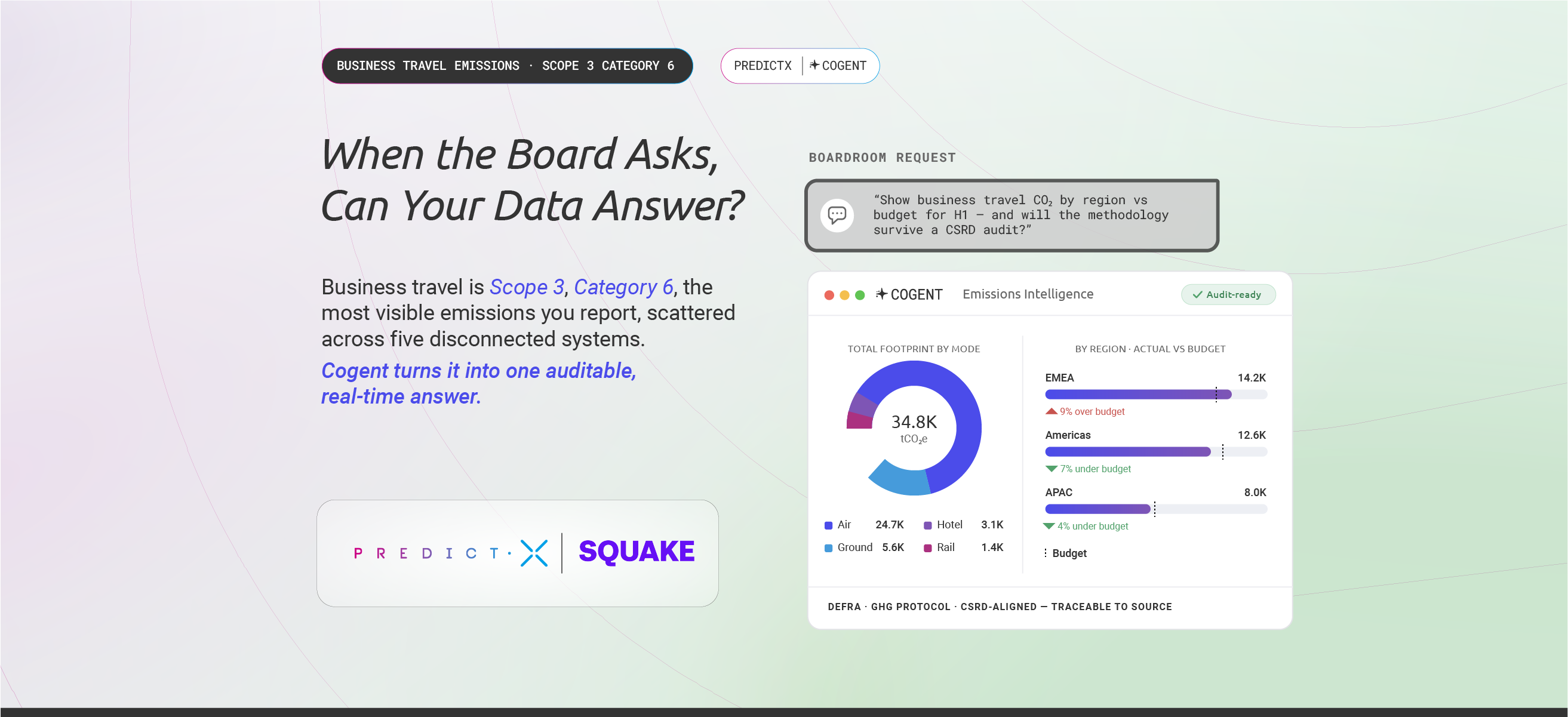

How does Cogent turn emissions data into a live intelligence layer?

Cogent by PredictX replaces the periodic emissions consolidation exercise with a live, queryable data layer so travel emissions can be interrogated alongside financial spend data in real time, without manual aggregation.

Cogent is not an expense management platform. It is an agentic AI for travel and expense that deploys AI agents to run investigations, surface patterns, and produce findings across consolidated T&E data. In the context of sustainability reporting, this means three capabilities that change how emissions are managed:

Multi-entity aggregation in a single query. Cogent aggregates CO2 data across the entire organisation, or any defined subset, instantly, with full reconciliation against the financial spend data sitting in the same layer.

Year-over-year and budget-vs-actual tracking. Comparing CO2 emissions for a specific region or entity against the prior year, or tracking performance against an annual budget, happens in seconds rather than weeks.

Cross-category emissions in one view. Air, hotel, rail, and ground transport emissions are queried together in the same conversation, giving a complete trip-level picture rather than a category-by-category patchwork.

What does auditable ESG reporting actually require from your T&E data?

Auditable ESG reporting for business travel requires four things: a single consistent emissions methodology applied across all transport modes, data traceable to source, reproducible query results, and the ability to update methodology retroactively without rebuilding the dataset from scratch.

Most manual processes fail on every one of these criteria. The methodology is assembled ad hoc across multiple systems. The data consolidation trail is a spreadsheet, not a data log. Results are not reproducible because they depend on who pulls the data and when. And if the methodology changes mid-year, the entire historical record must be rebuilt.

What an external auditor reviewing CSRD-compliant Scope 3 disclosures will look for:

- A named emissions factor standard applied consistently across all transport modes (e.g., DEFRA or an equivalent certified methodology)

- Source-level traceability: which booking, which entity, which period

- Methodology documentation that can be re-run to produce the same result

- Evidence that off-programme spend is captured, not just managed bookings

Cogent's emissions calculations are aligned with DEFRA, TIM, and the GHG Protocol, giving every query a defensible, auditor-ready methodology chain. As Keesup Choe describes it: "The solution moves your organisation from approximation to auditable precision, ensuring emissions data is verifiable for any review." For a detailed look at how that data chain works in practice, the audit-ready reporting and data chain of custody guide walks through exactly what auditability requires at the data level.

The CDP (Carbon Disclosure Project) and major ESG rating frameworks increasingly scrutinise not just the emissions figure reported, but the quality of the underlying data. A figure that cannot be independently validated will be rated lower than one that can, regardless of how ambitious the net zero target behind it is.

Want to test your hardest entity-level T&E question? Book a live Cogent demo and run it against real data.

Manual vs agentic: what do the two approaches actually produce?

The table below maps the two approaches across the criteria that matter for modern ESG disclosure and travel programme management.

No manual T&E emissions process was designed for CSRD-level scrutiny. The data is too fragmented, the methodology too inconsistent, and the consolidation process too slow to produce the auditable, real-time emissions picture that modern sustainability disclosure requires.

The most advanced programmes are moving beyond reporting entirely. Internal carbon pricing (ICP) converts CO2 metrics into a monetary value, typically a flat fee per tonne generated, so that sustainability performance becomes legible to finance stakeholders, not just sustainability teams. As Keesup Choe explains: "Calculating and offsetting carbon emissions from business travel is not enough to drive change. Companies are starting to introduce internal carbon pricing strategies to accelerate progress." Cogent's corporate travel sustainability platform supports ICP directly. For programmes targeting modal shift, the modal shift CO2 savings analysis provides a worked methodology for calculating and reporting the reduction.

The organisations that meet their net zero targets will not be the ones that simply travel less. They will be the ones whose data is good enough to act on.

Frequently Asked Questions

What is Scope 3 Category 6 emissions in the context of business travel?

Scope 3 Category 6 emissions cover all greenhouse gases produced by employees travelling for business purposes, including air, rail, ground transport, and hotel stays. Under the Greenhouse Gas Protocol Corporate Standard, companies are required to measure and report these as part of their indirect emissions inventory. For most large organisations, business air travel is the single largest Category 6 emissions source.

What is CSRD and does it apply to business travel emissions reporting?

The Corporate Sustainability Reporting Directive (CSRD) is EU legislation requiring large companies to publish auditable Scope 3 emissions disclosures, including Category 6 business travel. In-scope companies must verify these disclosures with an external auditor. Non-EU companies with significant EU operations or revenues are also covered under Phase 4, making CSRD a global compliance issue for enterprise travel programmes.

Why is calculating a corporate travel carbon footprint so difficult?

Calculating a corporate travel carbon footprint is difficult because air, hotel, rail, and ground transport each use different emissions factor methodologies, and the data for each mode sits in separate, disconnected systems. TMC booking data, corporate card feeds, expense platforms, and fleet management systems do not share a common format or update in sync, creating a manual consolidation burden that takes weeks and introduces error at every step.

How does Cogent handle Scope 3 emissions reporting for business travel?

Cogent by PredictX replaces the periodic emissions consolidation exercise with a live, queryable data layer where CO2 emissions across air, hotel, rail, and ground are interrogated in the same conversation as financial spend data. Multi-entity aggregation, budget-vs-actual tracking, and year-over-year comparisons run in minutes, not weeks. Every query produces an auditable, methodology-consistent output traceable to source.

What is the difference between ESG reporting and CSRD compliance for travel programmes?

ESG reporting is a broad term for voluntary or mandatory environmental, social, and governance disclosures; CSRD is a specific EU regulatory framework with mandatory scope, defined standards, and external audit requirements. CSRD compliance requires adherence to the European Sustainability Reporting Standards (ESRS), which specifically mandate Scope 3 Category 6 disclosure. Travel teams whose data cannot satisfy ESRS requirements face direct regulatory exposure.

Can agentic AI replace the manual process of building a travel emissions report?

Yes. An agentic T&E platform like Cogent replaces the manual data consolidation process by running emissions queries across a live, unified dataset rather than requiring analysts to pull, clean, and aggregate data from multiple systems. The result is an emissions report that is faster to produce, consistent in methodology, and audit-ready by design.

How can a company meet its net zero targets for business travel?

Meeting net zero targets for business travel requires accurate emissions measurement across all transport modes, a reduction strategy built on real data rather than estimates, and the ability to track progress against budget in real time, not just at year end. Organisations that rely on annual manual consolidation cannot course-correct mid-year. Those using a live data layer can identify carbon hotspots before they compound and model the impact of policy changes before implementing them. Reporting is not the goal. Reduction is. But reduction without accurate data is guesswork.

Ask one question your current sustainability reporting cannot answer

If your board asked today for business travel emissions by region, by entity, and against budget, how long would it take, and would the methodology hold up to an external auditor?

Cogent by PredictX handles that query in minutes. Explore what agentic AI for T&E reporting means for your programme, or request a Cogent demo and test it against your hardest sustainability question.

Related Posts

.webp)

Business Travel Emissions: The Hidden Data Gaps Putting Your Carbon Report at Risk

The What-If Machine: Using Travel Data & Predictive Analytics to Model Your Path to Net-Zero Targets

The Data Chain of Custody: Why Audit-Ready Reporting Begins with Consolidated T&E Data

PredictX x SQUAKE: Quantifying CO₂e Savings from Air-to-Rail Modal Shift for Audit-Ready CSRD and Scope 3

From Estimates to Evidence: PredictX x SQUAKE for Audit-Ready CO₂ Reporting

Failing Audits? Get the PredictX Product Sheet: The Path to Auditable Corporate Travel Emissions

The Scope 3 Mandate: Why CSRD Reporting Turns Business Travel Emissions into a Boardroom Issue

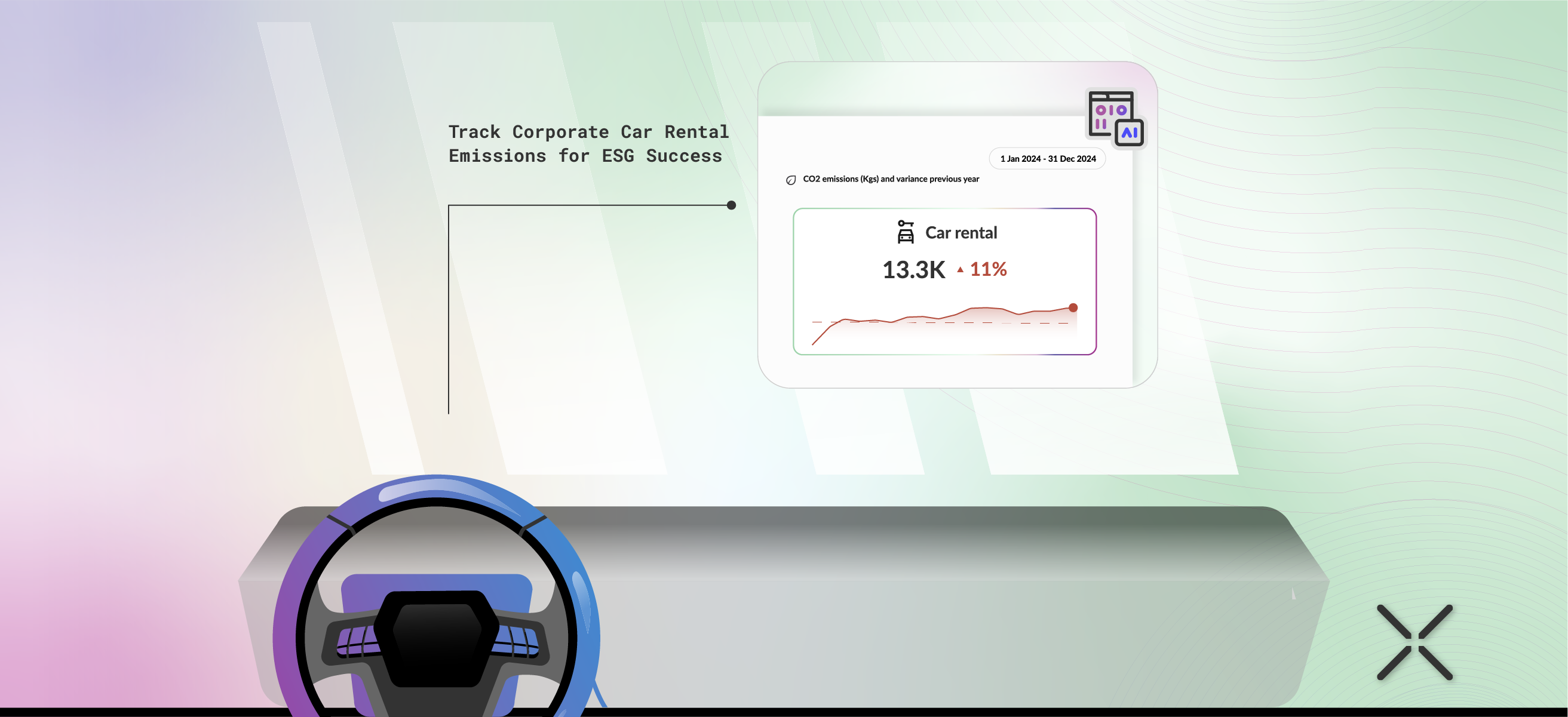

Putting Your Car Rental Emissions in the Driving Seat: A Smarter Approach to Sustainability

Beyond Flights: Your Guide to Tracking and Reducing Ground Transport Emissions

The Invisible Carbon Footprint: Why Your ESG Reporting Is Incomplete

.webp)

The 2025 Playbook for Net-Zero Business Travel by PredictX & SQUAKE: Your 4-Step Guide to Actionable Sustainability

PredictX and SQUAKE Make ESG Sustainability Goals Measurable and Audit-Ready for Corporate Travel Management

%20(23).png)

PredictX for Sustainability

.png)

How To Promote Sustainability and Calculate Your Company's Carbon Footprint

%20(1).png)

How PredictX is Pioneering the Use of AI for Corporate Travel Sustainability

.png)

Adhering to the CSRD: Shaping the Future of Corporate Travel Sustainability with PredictX

Unveiling PredictX’s Internal Carbon Pricing Tool: A Transformative Leap for Business Travel Sustainability

Unlocking Net Zero Goals in Corporate Travel: Insights from PredictX at ITM Sustainability Showcase 2024 Webinar